$130 billion poured into AI startups in 2026. Sounds massive — until you realize more AI companies crashed and burned this year than the last three years combined.

The biggest rounds got obscenely bigger. The smallest startups got starved out. And somewhere in the middle, hundreds of well-funded companies quietly vanished while nobody was paying attention.

This AI startup funding report cracks open every number behind the headlines — who actually raised, which sectors VCs fought over, which ones they abandoned, and where all that venture capital really ended up. Seed to mega-round. Silicon Valley to the Middle East. Foundation models to humanoid robots.

No sugarcoating. No recycled stats. Just the raw funding map of 2026 — with receipts.

Total AI Startup Funding Report in 2026

How Much Money Actually Moved

Global AI startup funding crossed $130 billion in 2026 — a sharp jump from $97 billion in 2025. But zoom into the quarters and the picture gets messier:

| Quarter | Estimated Funding | What Happened |

|---|---|---|

| Q1 | ~$38B | Late-2025 mega-round momentum spilled over |

| Q2 | ~$28B | Seasonal cooldown, valuation standoffs |

| Q3 | ~$31B | Enterprise AI traction pulled capital back in |

| Q4 | ~$35B | Pre-IPO frenzy, late-stage stacking |

2023 was the reset. 2024 was cautious re-entry. 2025 brought institutional confidence back. 2026 drew a hard line between the funded and the finished.

Fewer Checks, Bigger Bets — The Barbell Effect

Deal count dropped ~14%. Total capital went up. That’s not a contradiction — that’s a market screaming concentration.

The barbell effect is in full swing. Mega-rounds above $500M at one end. Sub-$3M micro-rounds at the other. The middle is collapsing — and Series A/B startups without hard revenue metrics are stuck in a dead zone with no follow-on in sight.

Public Markets Set the Tone for Private Money

Strong AI stock returns gave crossover investors the green light to jump back into private deals. The IPO window — sealed shut since 2022 — finally cracked open mid-2026. SPACs? Still dead. Nobody’s resurrecting that playbook for AI.

AI Funding by Stage in 2026

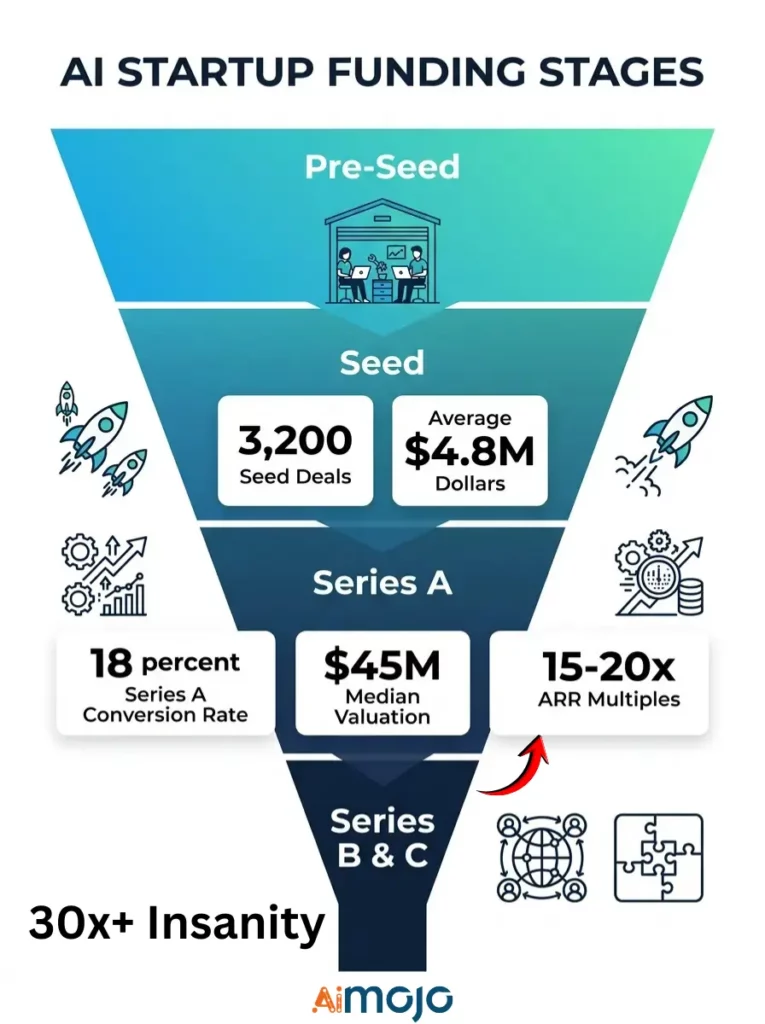

Pre-Seed & Seed: The Garage-Stage AI Bets

Around 3,200 seed-stage AI deals closed globally. Average round size for AI-native startups: $4.8M, up from $3.5M in 2024. Top seed investors — Y Combinator, Sequoia Scout, and a growing army of AI-specific micro-VCs — drove the action. San Francisco, London, Bangalore dominated the map.

Series A: The First Real Stress Test

Seed-to-Series A conversion rate: roughly 18%. Down from 24% in 2024. The bar moved drastically — investors now demand $1M+ ARR, net revenue retention above 120%, and a moat that goes deeper than a prompt chain. Median pre-money valuation for AI Series A rounds: ~$45M. Miss the benchmarks? Dead silence from every partner on Sand Hill Road.

Series B & C: Scaling or Stalling?

The Series B crunch crushed startups in oversaturated verticals — AI writing assistants, generic chatbot shells, copycat productivity tools. Revenue multiples compressed to 15–20x ARR, down from the 30x+ insanity of 2023. Investors grilled founders on gross margins, churn, and unit economics. The “we’ll monetize later” pitch officially expired.

Late Stage, Growth Equity & Mega-Rounds: The $500M+ Club

At least 11 AI rounds blew past the $500M mark this year. Sovereign wealth funds, crossover hedge funds, and corporate strategics piled in aggressively. Secondary market activity for pre-IPO AI equity hit record highs. If you were already winning, capital came hunting for you.

Which AI Sectors Got Flush With Cash

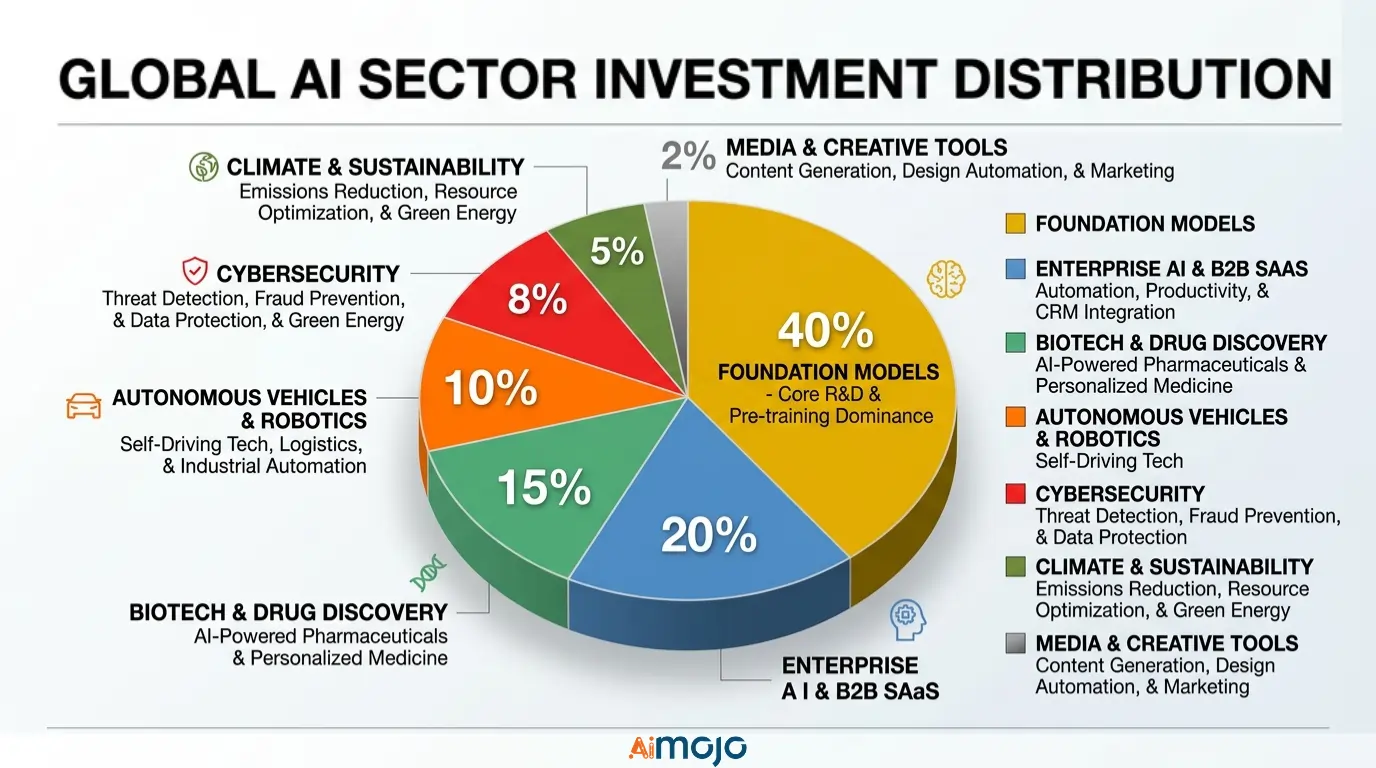

Foundation Models & Large Language Models — Still the Darling or Fading Fast?

Still dominant, but dangerously top-heavy. The top five foundation model companies swallowed over 40% of all LLM-specific funding. New entrants couldn’t raise without an extremely sharp differentiation story. Open-weight model startups, riding the DeepSeek momentum, attracted smaller but committed investor pools.

Enterprise AI & B2B SaaS — The Quiet Cash Machine

Zero fanfare. Consistent checks. Vertical SaaS with AI-native workflows — legal, procurement, compliance, logistics — raised round after round. AI copilot and autonomous agent startups saw a surge, though investor patience for long enterprise sales cycles is wearing thin.

Biotech & Drug Discovery

FDA-pathway AI companies with clinical-stage assets commanded premium valuations over pre-clinical peers. Big pharma corporate venture arms — Novo Holdings, Roche Venture Fund, Amgen Ventures — wrote increasingly aggressive checks into computational drug discovery.

AI for Fintech, Insurance & Risk

Steady, not explosive. Fraud detection, automated underwriting, and compliance AI raised well. Regulatory tailwinds helped — governments want better risk infrastructure and they’re willing to buy it.

Autonomous Vehicles, Robotics & Physical AI

The noisiest sector of the year. Humanoid robotics pulled multiple $200M+ rounds — serious institutional money, not just speculative hype. Warehouse automation, delivery bots, and autonomous trucking attracted strategic capital from logistics operators who can’t afford to sit out.

AI in Cybersecurity

Hot across every stage. Threat detection, automated response, vulnerability scanning — all well-funded. Government and defense contracts acted as a direct funding accelerant.

AI for Climate, Energy & Sustainability

ESG-mandated capital flowed into carbon tracking, grid optimization, and materials science AI. Smaller average round sizes, but high deal count and growing investor interest.

AI in Media, Creative Tools & Entertainment

Cooling fast. Copyright litigation risk spooked investors. The survivors: creator-economy tools with proper licensing frameworks and real paying users — not just viral demos.

The VCs, Corporates, and Sovereign Funds Shaping AI Startup Funding in 2026

Top 20 Most Active AI Venture Capital Firms

Andreessen Horowitz, Sequoia, Lightspeed, Accel, Index Ventures, Khosla Ventures, Founders Fund — still leading by deal count.

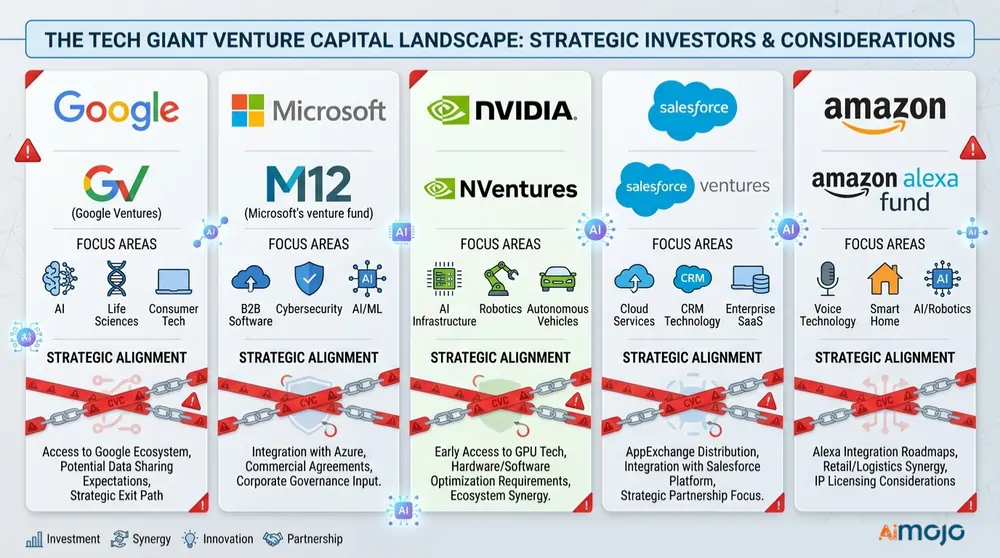

Corporate Venture Arms With the Biggest AI Footprints

Google Ventures, Microsoft’s M12, Nvidia’s NVentures, Salesforce Ventures, Amazon’s Alexa Fund — all ramped up AI deal activity. But founders, read the fine print. Corporate money always comes with strings. In 2026, those strings got tighter, more binding, and harder to negotiate out of.

Sovereign Wealth Funds and Government-Backed Capital

Saudi Arabia’s PIF, Abu Dhabi’s Mubadala and MGX, Singapore’s GIC and Temasek — all wrote nine-figure checks into AI rounds this year. This is the story most funding reports underplay.

On the U.S. side, In-Q-Tel, NSF-backed programs, and CHIPS Act spillover money created a parallel funding pipeline for defense-relevant and semiconductor AI startups. EU AI Act enforcement pushed European government-backed funds toward “safe” compliance-focused AI over frontier research.

Angel Investors & Micro-VCs — The Scrappy First Checks

Don’t overlook this tier. AI-focused solo GPs running sub-$50M funds filled a critical gap for technical founders in niche domains. Angel syndicates on AngelList moved faster than institutional funds stuck in committee cycles — and that speed mattered.

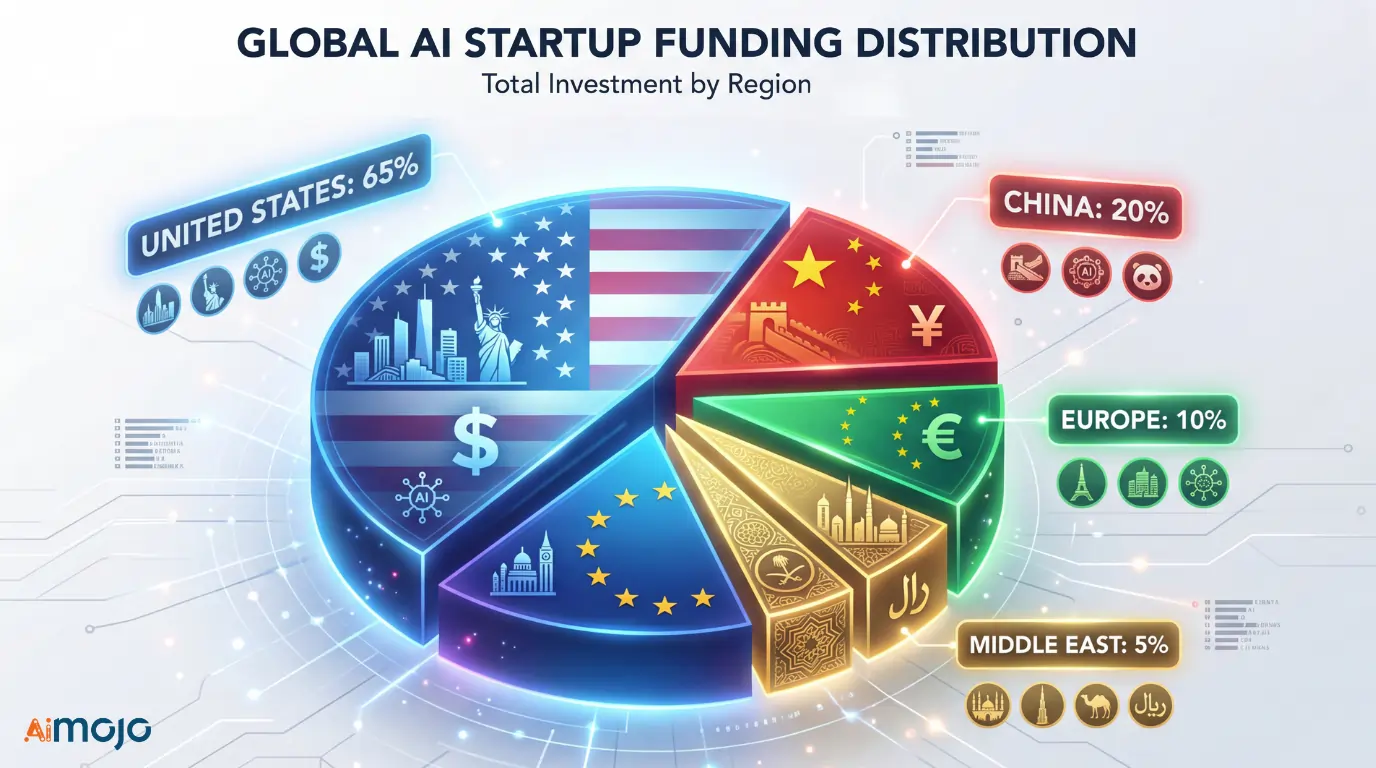

AI Startup Funding by Region

🇺🇸 United States — Still the heavyweight champion. Roughly 65% of global AI funding landed here. Bay Area leads, but New York, Austin, Seattle, and Miami all grabbed bigger slices. Texas and Florida state-level incentives are actively pulling AI startups out of California.

🇨🇳 China — Government-directed capital focused on semiconductor self-sufficiency and domestic LLM development. U.S. chip export restrictions dictated which startups got funded and which got choked out.

🇪🇺 Europe — Punching below its weight relative to talent. EU AI Act compliance costs hit smaller startups hardest. London stood apart as the clear outlier with a well-funded, fast-moving AI scene. France and Germany showed muscle in industrial AI applications.

🇦🇪 Middle East — UAE and Saudi Arabia positioned themselves as the new power players, funding AI megaprojects and rolling out startup visa incentives that poached founders from Europe and South Asia.

🇮🇳 India, Southeast Asia & Latin America — High growth, lower ticket sizes. Applied AI in fintech, agriculture, and logistics drove deal volume across all three regions.

AI Startup Valuations in 2026

Median and Mean Valuations by Stage

| Stage | Median Pre-Money | YoY Shift |

|---|---|---|

| Seed | ~$15M | ↑ 18% |

| Series A | ~$45M | ↑ 10% |

| Series B | ~$150M | ↓ 5% |

| Series C+ | $300M–$2B+ | All over the map |

AI startups still carry a 30–50% valuation premium over non-AI tech at the same stages — but that spread is narrowing fast.

Down Rounds, Flat Rounds & the Recaps Nobody Talks About

An estimated 20–25% of AI startups raising follow-on capital took a valuation cut. Most never made headlines. Structured terms became standard at Series B and beyond — participating preferred, ratchets, pay-to-play provisions. Press releases showed up rounds. Term sheets told a different story.

Revenue Multiples Investors Actually Paid

Growth-stage AI SaaS multiples compressed to 18–25x ARR. Down from the 40x+ some companies commanded in 2023. The “AI label” premium still exists, but it now requires proof of retention and expansion revenue — not just a pitch deck with the word “intelligence” on every slide.

SAFEs, Convertible Notes & Non-Priced Rounds in AI

SAFEs remained the dominant seed-stage instrument. Valuation caps crept higher alongside round sizes, reflecting the hard reality that AI-native companies simply cost more to build at inception than traditional SaaS.

The AI Startups That Burned Through Cash and Hit a Wall in 2026

Notable AI Startup Shutdowns and Acqui-Hires

Multiple companies with $50M+ in total funding shut down or got absorbed this year.

The pattern was painfully consistent: compute costs ballooned, post-trial customers churned, and defensibility vanished the moment foundation model providers added the same features natively.

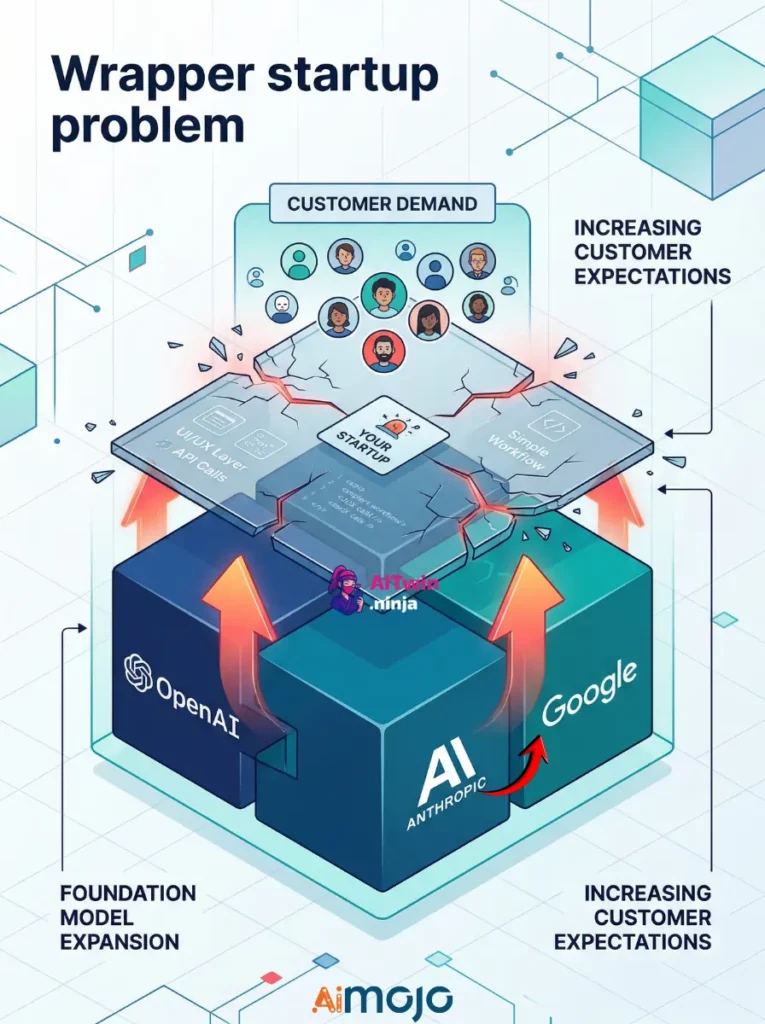

The “Wrapper” Reckoning — When a Thin API Layer Isn’t a Business

The most predictable wipeout of the year. Startups built as thin layers on OpenAI, Anthropic, or Google APIs watched their reason to exist disappear overnight.

VC sentiment turned hostile toward wrappers in mid-2025. By 2026, the money was gone.

Burn Rate Benchmarks — How Fast AI Startups Spend

Numbers most founders don’t want to see:

Fourteen months. In a market where Series A rounds take 6–9 months to close, that math should terrify every pre-revenue AI founder reading this.

AI Startup Exits in 2026

Major AI Acquisitions of 2026

Big Tech acqui-hires — talent grabs packaged as acquisitions — made up most exits by count. But several strategic deals in the $500M–$2B range closed in enterprise AI and cybersecurity, proving real product value is getting recognized and paid for.

AI IPOs and Direct Listings

A handful of AI companies filed S-1s. Post-IPO performance was mixed. The pipeline for late 2026 and into 2027 is the strongest since 2021 — but public market investors are asking harder questions than their private-side counterparts ever did.

Secondary Market Sales — Insiders Cashing Out Early

Secondary transaction volume for AI startup shares surged. Insiders are seeking liquidity well before any IPO — and secondary market pricing often tells a more honest valuation story than the last priced round ever will.

How AI Regulation Is Redirecting Startup Capital

U.S. Executive Orders, Congressional Bills & State-Level AI Laws

U.S. executive orders on AI safety, chip export controls, and expanded federal AI procurement budgets all steered capital toward defense AI and domestic compute infrastructure. Policy isn’t just politics here — it’s allocation strategy.

EU AI Act — One Year In

Compliance costs hit smaller startups hardest. The counterargument gaining traction: companies that absorb these costs now hold a regulatory moat competitors can’t afford to cross. Advantage or death sentence — depends entirely on your burn rate.

China’s AI Governance Model

Beijing’s rules funneled capital toward state-sanctioned priorities: domestic large language models, chip self-sufficiency, and surveillance-adjacent applications.

Global AI Safety Summits and International Coordination Efforts

Frontier model funding appetite felt the squeeze. Some investors openly avoided companies flagged as high-risk under global safety frameworks — not from moral conviction, but because regulatory uncertainty made return modeling nearly impossible.

AI Startup Funding Forecast

Bull Case, Base Case, Bear Case — Three Funding Scenarios

| Scenario | Projection | Key Driver |

|---|---|---|

| 🟢 Bull | $150B+ | IPO window widens, agentic AI hype peaks |

| 🟡 Base | $130–140B | Concentrated at extremes, steady institutional flow |

| 🔴 Bear | Below $110B | Market correction, geopolitical shock, compute spike |

Sectors Poised to Absorb the Most Capital Next

Autonomous AI agents. Defense AI. AI-for-science. Edge computing. Infrastructure tooling. If you’re building in any of these, your fundraising window just got shorter — in a good way.

The “AI Bubble” Debate — Honest Assessment With Receipts

Foundation model valuations carry dot-com-era risk profiles. Enterprise AI with proven recurring revenue is just well-margined software. Lumping both into the same “bubble” label is lazy and financially reckless.

Advice for Founders Raising in This Market

What VCs are pattern-matching on right now:

✅ Gross margins above 70%

✅ Customer retention past the pilot phase

✅ Technical moat deeper than a prompt chain

✅ Capital efficiency over growth-at-all-costs storytelling

Ditch the TAM slide. Every investor has seen the same “$X trillion” chart. Show the receipts instead.

Sources & Disclaimer

This report compiles and analyzes publicly available AI startup funding data from industry-leading databases, published investor reports, regulatory filings, and verified media coverage. Figures represent estimates based on disclosed information and may not capture undisclosed or delayed deals. This report is intended for informational purposes and should not be treated as financial advice.

BONUS: Get our $200 “AI Mastery Toolkit” FREE when you sign up!

BONUS: Get our $200 “AI Mastery Toolkit” FREE when you sign up!